2026 Social Security Benefit Adjustments: Your Guide to Retirement Income Planning

Anúncios

Understanding your retirement income is paramount, and for millions of Americans, Social Security benefits form a critical pillar of that financial security. As we look towards the future, specifically to 2026 Social Security Adjustments, it’s crucial to be informed about potential changes and how they might impact your financial planning. This comprehensive guide aims to shed light on what to expect, how these adjustments are determined, and what steps you can take to ensure your retirement income remains robust.

Social Security is more than just a government program; it’s a promise of financial assistance to retirees, disabled workers, and survivors. Its stability and longevity are constantly under review, leading to periodic adjustments that can significantly affect recipients’ monthly checks. The year 2026 is on the horizon, and with it comes the anticipation of new calculations and modifications that could influence your future financial landscape. This article will delve into the intricacies of these potential changes, offering practical insights and actionable strategies for effective retirement income planning.

Anúncios

The Foundation: How Social Security Benefits Are Calculated

Before we can fully grasp the implications of 2026 Social Security Adjustments, it’s essential to understand the fundamental mechanics of how these benefits are initially calculated. Your Social Security benefit is not a flat rate; it’s a personalized calculation based on several factors, primarily your earnings history. The Social Security Administration (SSA) uses a formula that takes into account your 35 highest-earning years. These earnings are then indexed to account for changes in average wages over time, ensuring that earlier earnings reflect their value in today’s economy.

The Average Indexed Monthly Earnings (AIME)

The first step in determining your benefit is calculating your Average Indexed Monthly Earnings (AIME). This involves taking your indexed earnings for your 35 highest-earing years, summing them up, and then dividing by 420 (the number of months in 35 years). The AIME is a crucial figure because it directly feeds into the primary insurance amount (PIA) formula.

Anúncios

The Primary Insurance Amount (PIA)

Your Primary Insurance Amount (PIA) is the benefit you would receive if you start collecting Social Security at your full retirement age (FRA). The PIA is determined by applying a progressive formula to your AIME. This formula is progressive because it replaces a higher percentage of earnings for lower-income workers than for higher-income workers. The formula uses bend points, which are dollar amounts that change annually. For 2026, these bend points will be updated, potentially shifting the PIA calculation for new retirees.

Full Retirement Age (FRA)

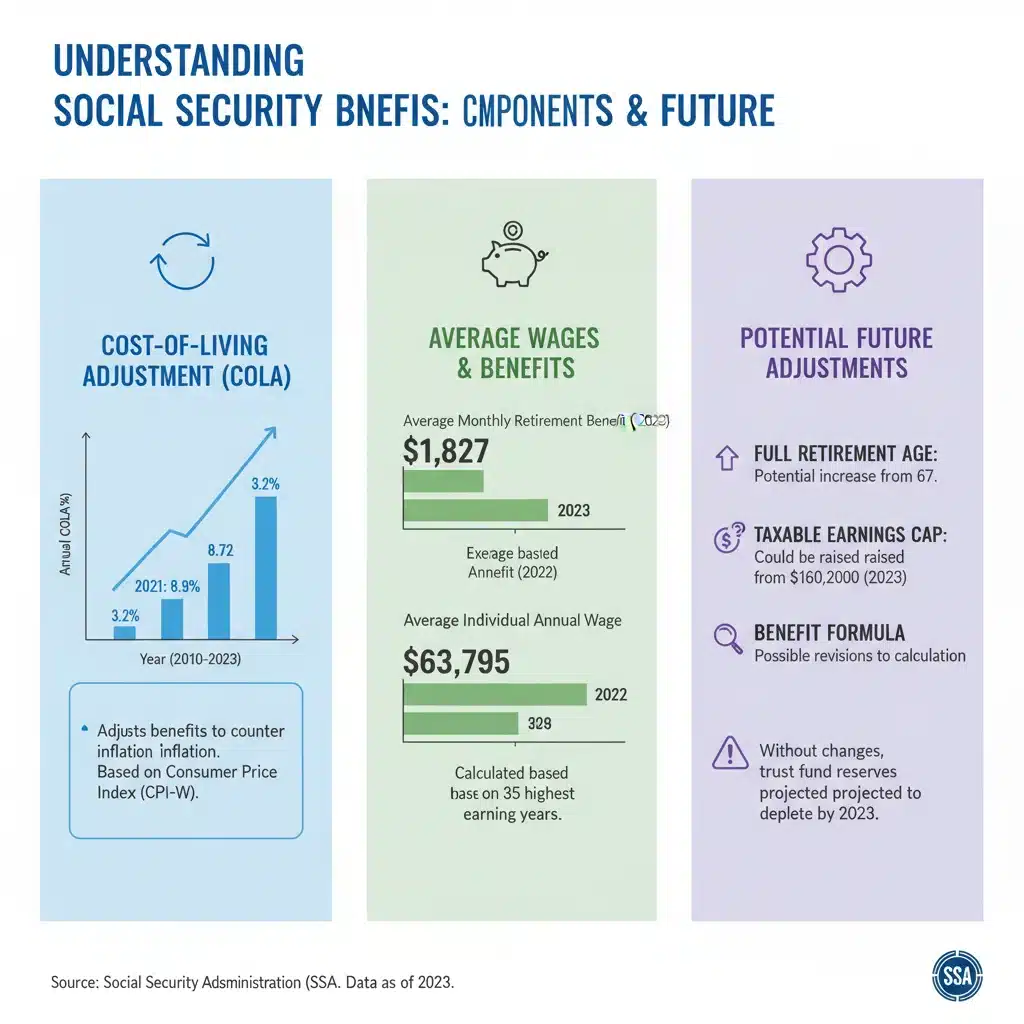

Your full retirement age (FRA) is a critical factor. It’s the age at which you’re entitled to receive 100% of your PIA. FRA varies depending on your birth year. For those born in 1960 or later, the FRA is 67. Claiming benefits before your FRA results in a permanent reduction, while delaying benefits past your FRA (up to age 70) can lead to increased benefits through delayed retirement credits. Understanding your FRA is vital for optimizing your 2026 Social Security Adjustments.

Key Drivers of 2026 Social Security Adjustments

Several economic and demographic factors influence the annual adjustments to Social Security benefits. For 2026 Social Security Adjustments, these same drivers will be at play, shaping the financial outlook for millions of beneficiaries. The most prominent of these is the Cost-of-Living Adjustment (COLA), but other factors like average wage index and legislative changes also play a significant role.

Cost-of-Living Adjustment (COLA)

The Cost-of-Living Adjustment (COLA) is perhaps the most anticipated annual adjustment for Social Security recipients. COLA is designed to ensure that the purchasing power of Social Security benefits is not eroded by inflation. It’s calculated based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) for the third quarter of the previous year. If the CPI-W increases, benefits receive a corresponding increase. If there’s no increase or a decrease in the CPI-W, there’s no COLA, though benefits will not decrease.

For 2026 Social Security Adjustments, the COLA will be determined by inflation trends observed in late 2025. Economic forecasts and current inflationary pressures will give us early indications, but the official announcement typically comes in October of the preceding year. A higher COLA means more purchasing power for retirees, while a lower COLA or no COLA will require more careful budgeting.

Average Wage Index (AWI)

The Average Wage Index (AWI) is another crucial factor, particularly for those who are still working and whose future benefits are being calculated. The AWI reflects the average wages of all workers in the U.S. and is used to index earnings records for benefit calculations and to adjust various thresholds, such as the bend points in the PIA formula and the Social Security earnings limit. A higher AWI generally means higher future benefits for those still accumulating work credits.

The AWI for 2026 Social Security Adjustments will impact new retirees and those who have not yet claimed benefits. It helps ensure that the benefits reflect the general wage growth in the economy, preventing the erosion of future retirement income due to stagnant indexed earnings.

Legislative and Policy Changes

While COLA and AWI are standard annual adjustments, legislative and policy changes can also significantly impact Social Security. These changes are less frequent but can have a more profound and long-lasting effect. Debates about the long-term solvency of Social Security often lead to discussions about raising the full retirement age, adjusting the COLA formula, or altering the taxation of benefits.

As we approach 2026, it’s always prudent to keep an eye on congressional discussions regarding Social Security reform. Any legislative action could introduce new parameters for 2026 Social Security Adjustments, potentially altering the benefit structure for current and future retirees. While such changes are often contentious and slow-moving, they are a vital consideration for long-term financial planning.

Anticipating the Impact of 2026 Social Security Adjustments

For current retirees, the primary impact of 2026 Social Security Adjustments will likely be through the COLA, affecting their monthly benefit amount. A higher COLA can provide a welcome boost to income, helping to offset rising costs of living. Conversely, a lower COLA might necessitate tighter budgeting or reliance on other retirement savings.

For those nearing retirement or still in their working years, the impact could be broader. Changes to the AWI will influence their future PIA calculations, while any legislative reforms could alter the rules for claiming benefits, the full retirement age, or the overall benefit structure. It’s crucial to stay informed and adapt your retirement planning strategies accordingly.

Impact on Current Beneficiaries

Current beneficiaries will primarily experience the effects of the COLA. An increase in benefits, even a modest one, can make a difference in covering daily expenses, healthcare costs, and discretionary spending. It’s important to remember that while COLA helps maintain purchasing power, it might not always fully align with individual spending patterns, especially for specific categories like healthcare, which often outpace general inflation.

Therefore, even with a favorable COLA for 2026 Social Security Adjustments, retirees should continue to monitor their expenses and ensure their overall financial plan remains sound.

Impact on Future Beneficiaries

Future beneficiaries, including those still working, face a more complex set of potential impacts. The AWI’s trajectory will influence their initial benefit calculations. Furthermore, any legislative changes regarding the full retirement age or benefit formulas could significantly alter their expected Social Security income. This uncertainty underscores the importance of a diversified retirement savings strategy, not solely relying on Social Security.

Understanding these potential shifts is key to proactive planning. For instance, if the full retirement age were to increase, individuals might need to adjust their planned retirement dates or increase other savings to bridge the gap.

Strategies for Optimizing Your Retirement Income

Regardless of the specifics of 2026 Social Security Adjustments, there are timeless strategies you can employ to optimize your retirement income and build a more secure financial future. These strategies focus on maximizing your Social Security benefits, diversifying your savings, and managing your expenses effectively.

Maximizing Your Social Security Benefits

Even within the existing framework, there are ways to maximize your Social Security benefits:

- Work Longer: Each year you work past your 35 highest-earning years can replace a lower-earning year in your calculation, potentially increasing your AIME and thus your PIA.

- Delay Claiming: For every year you delay claiming benefits past your full retirement age, up to age 70, you earn delayed retirement credits, which permanently increase your monthly benefit. This can be a significant boost, especially if you have other income sources to rely on in the interim.

- Coordinate with Spouse: If you are married, understanding spousal and survivor benefits can lead to a higher combined household income. Strategic claiming decisions can optimize benefits for both partners.

- Monitor Earnings Record: Regularly check your Social Security earnings record for accuracy. Errors can lead to lower benefits, so it’s vital to correct any discrepancies promptly.

Diversifying Your Retirement Savings

Relying solely on Social Security for retirement income is often insufficient. A diversified approach is crucial:

- 401(k)s and IRAs: These tax-advantaged retirement accounts are powerful tools for accumulating wealth. Maximize your contributions, especially if your employer offers a matching program.

- Personal Savings and Investments: Beyond dedicated retirement accounts, consider taxable brokerage accounts, real estate, or other investments to create additional income streams.

- Annuities: For some, annuities can provide a guaranteed income stream in retirement, complementing Social Security benefits.

Effective Expense Management

Controlling your expenses is just as important as maximizing your income. As 2026 Social Security Adjustments come into play, a clear understanding of your budget will be invaluable:

- Create a Detailed Budget: Understand where your money goes. Categorize expenses and identify areas where you can cut back without sacrificing your quality of life.

- Reduce Debt: Entering retirement debt-free, especially from high-interest credit card debt, can significantly reduce financial stress and free up income.

- Plan for Healthcare Costs: Healthcare is a major expense in retirement. Explore Medicare options, Medigap policies, and potentially long-term care insurance to mitigate these costs.

The Role of Financial Planning in Navigating 2026 Social Security Adjustments

Navigating the complexities of Social Security and planning for future adjustments, such as those anticipated in 2026 Social Security Adjustments, can be daunting. This is where professional financial planning becomes invaluable. A qualified financial advisor can help you assess your current situation, project future income and expenses, and develop a personalized strategy to meet your retirement goals.

Personalized Benefit Analysis

A financial advisor can provide a personalized analysis of your Social Security benefits, taking into account your earnings history, claiming age options, and spousal benefits. They can run different scenarios to show you the impact of claiming at various ages and help you determine the optimal strategy for your unique circumstances.

Holistic Retirement Planning

Beyond Social Security, a financial planner can assist with holistic retirement planning, integrating all your income sources, investments, and expenses into a comprehensive plan. This includes tax planning, estate planning, and risk management, ensuring all aspects of your financial life are aligned with your retirement objectives.

Adapting to Changes

The financial landscape is constantly evolving, and Social Security is no exception. A good financial advisor will keep you informed about potential policy changes and economic shifts that could impact your retirement. They can help you adapt your plan as needed, ensuring you remain on track even in the face of unexpected 2026 Social Security Adjustments or other developments.

Common Misconceptions About Social Security Adjustments

Many myths and misunderstandings surround Social Security, particularly regarding benefit adjustments. Dispelling these can help you make more informed decisions about your retirement planning and better prepare for 2026 Social Security Adjustments.

Myth 1: Social Security Will Run Out

While Social Security faces long-term financial challenges, it is not projected to ‘run out.’ The program is funded by dedicated payroll taxes, and even if no legislative action is taken, it would still be able to pay a significant portion of promised benefits. The concern is about the ability to pay 100% of scheduled benefits in the distant future, which is why adjustments and reforms are continually discussed.

Myth 2: COLA Always Keeps Up with My Personal Inflation

The COLA is based on the CPI-W, a broad measure of inflation for urban wage earners and clerical workers. While it generally reflects price changes, it may not perfectly align with every individual’s spending patterns. For instance, if your personal healthcare costs rise significantly faster than the CPI-W, the COLA might not fully cover that increase. This highlights the importance of personal budgeting and additional savings.

Myth 3: My Benefits will Automatically Increase if I Keep Working

While working longer can increase your benefits by replacing lower-earning years in your AIME calculation, it’s not always an automatic increase. If your current earnings are lower than your indexed past earnings, working more years might not significantly boost your average. The most impactful way to increase benefits by working longer is to delay claiming past your FRA, earning delayed retirement credits.

The Future Outlook for Social Security and 2026 Adjustments

The long-term solvency of Social Security is a perennial topic of discussion among policymakers and economists. Demographic shifts, including longer life expectancies and lower birth rates, contribute to the challenges facing the program. As we look towards 2026 Social Security Adjustments and beyond, it’s likely that discussions around various reform proposals will continue.

Potential Reform Scenarios

Some common reform proposals include:

- Raising the Full Retirement Age: Gradually increasing the age at which individuals can claim their full benefits.

- Adjusting the COLA Formula: Changing the index used to calculate the COLA, potentially to one that reflects inflation experienced by seniors more accurately (e.g., CPI-E), or one that results in lower annual increases.

- Increasing the Social Security Tax Cap: Applying Social Security taxes to a higher amount of earnings or eliminating the cap altogether.

- Increasing the Payroll Tax Rate: A direct increase in the percentage of earnings contributed to Social Security.

- Means-Testing Benefits: Reducing benefits for higher-income retirees.

While none of these are guaranteed for 2026 Social Security Adjustments, they highlight the ongoing efforts to ensure the program’s financial health for future generations. Staying informed about these debates is an important part of comprehensive retirement planning.

Conclusion: Proactive Planning for 2026 Social Security Adjustments

The anticipation of 2026 Social Security Adjustments serves as a timely reminder of the dynamic nature of retirement income planning. While the specifics of these adjustments are yet to be fully known, understanding the underlying mechanisms of Social Security, the factors influencing its changes, and the strategies available to you can empower you to make informed decisions.

Whether you are a current beneficiary or still decades away from retirement, proactive planning is your best defense against uncertainty. Maximize your benefits by making strategic claiming decisions, diversify your savings beyond Social Security, and manage your expenses diligently. Consulting with a qualified financial advisor can provide invaluable guidance, offering personalized insights and helping you navigate the complexities of Social Security and broader retirement planning.

By taking these steps, you can build a robust financial foundation that withstands potential adjustments and ensures a more secure and comfortable retirement for years to come. Don’t wait for the official announcements; start planning today to secure your financial future.