Navigating 2026 US Tax Law Changes: Investor’s Essential Guide

Anúncios

The financial world is constantly evolving, and for investors in the United States, staying abreast of impending tax law changes is not merely good practice – it’s an absolute necessity. As we look towards 2026, a series of significant adjustments to the US tax code are on the horizon, poised to reshape investment strategies and impact portfolio returns. These changes, stemming from various legislative actions and sunset provisions of previous laws, demand careful attention and proactive planning. Understanding the nuances of these 2026 US Tax Changes is paramount for optimizing your financial position and ensuring compliance.

The Tax Cuts and Jobs Act (TCJA) of 2017, a landmark piece of legislation, introduced a plethora of changes, many of which were temporary. A significant number of its individual tax provisions are set to expire at the end of 2025, paving the way for a return to pre-TCJA rules or the introduction of new legislation. This impending shift creates both challenges and opportunities for investors. From adjustments to individual income tax rates and brackets to potential alterations in capital gains taxes, estate taxes, and deductions, the scope of these changes is broad and far-reaching. This comprehensive guide aims to dissect the most critical 2026 US Tax Changes that every investor needs to understand, providing insights and actionable strategies to navigate the evolving tax landscape.

Anúncios

The Sunset of TCJA Provisions: What’s Reverting in 2026?

One of the most impactful aspects of the upcoming 2026 tax landscape is the scheduled expiration of many provisions from the Tax Cuts and Jobs Act of 2017. When the TCJA was enacted, a political compromise led to many individual tax cuts being temporary, set to ‘sunset’ after 2025. This means that, without new legislative action, a return to pre-TCJA tax law is the default. For investors, this includes a range of critical areas that could directly affect their taxable income and investment returns.

Individual Income Tax Rates and Brackets

Perhaps the most widely felt change will be the reversion of individual income tax rates and brackets. The TCJA lowered marginal tax rates across most brackets. In 2026, these rates are expected to rise. For instance, the top individual income tax rate, which was reduced from 39.6% to 37% by the TCJA, is projected to revert to 39.6%. Similarly, other brackets will see increases. This means that ordinary income from investments, such as interest from bonds, non-qualified dividends, and short-term capital gains, will be taxed at higher rates. Investors should assess their income streams and consider strategies to defer income or realize gains in lower-tax environments if possible before 2026.

Anúncios

Standard Deduction and Personal Exemptions

The TCJA significantly increased the standard deduction, nearly doubling it for many filers, while simultaneously eliminating personal exemptions. In 2026, the standard deduction amounts are expected to revert to their pre-TCJA levels (adjusted for inflation), and personal exemptions could be reinstated. This combination could alter the tax liability for many, especially those who previously itemized or benefited greatly from the larger standard deduction. Investors should review their itemized deductions versus the standard deduction to understand the potential impact on their taxable income.

State and Local Tax (SALT) Deduction Cap

A contentious provision of the TCJA was the $10,000 cap on the deduction for state and local taxes (SALT). This cap significantly impacted residents in high-tax states. While there has been ongoing debate and proposals to repeal or modify this cap, it is also set to expire in 2026. If it simply expires without new legislation, the SALT deduction could become unlimited again, which would be a substantial benefit for many investors in states with high property and income taxes. This change could influence decisions regarding residency or investment property locations.

Capital Gains and Qualified Dividends: A Critical Look for Investors

For investors, capital gains and qualified dividends are often at the heart of their taxable income. The 2026 US Tax Changes could bring significant shifts to how these are taxed, directly impacting investment returns and strategies.

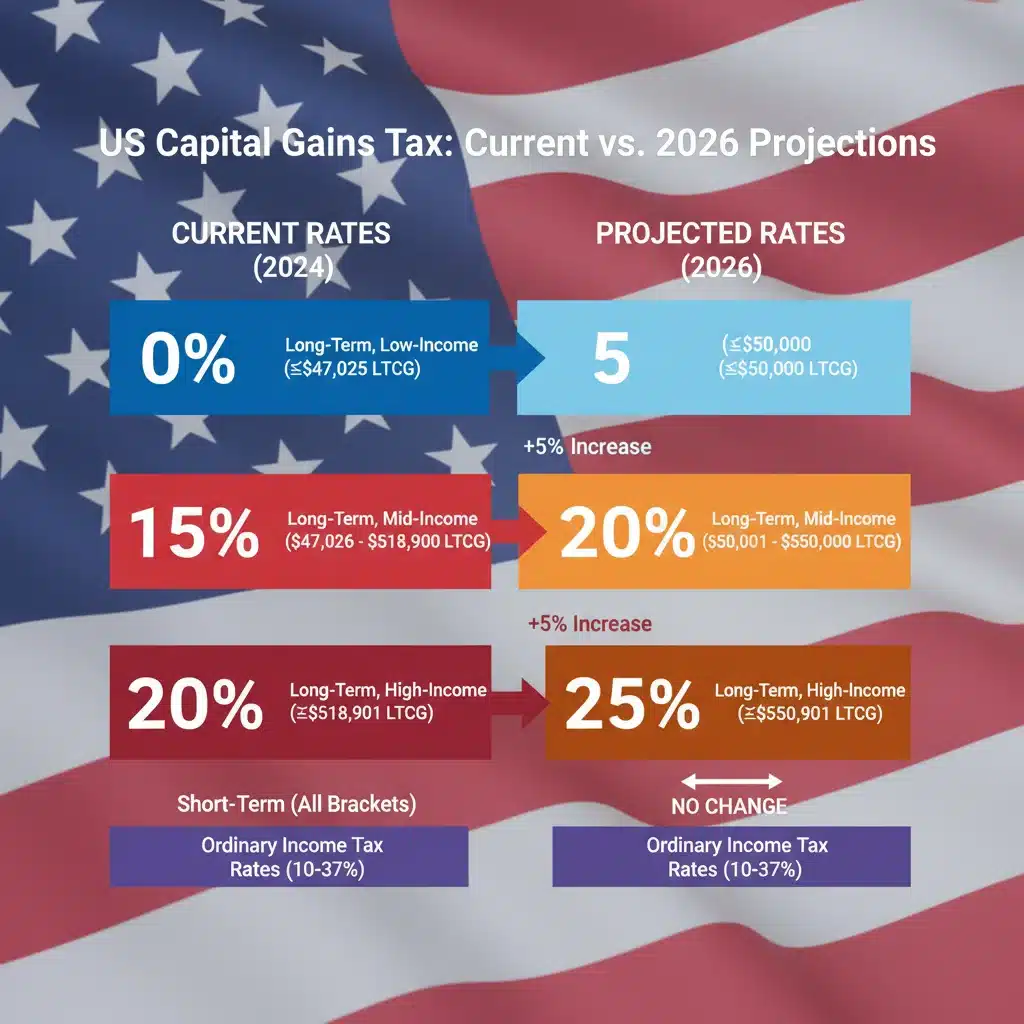

Long-Term Capital Gains and Qualified Dividend Rates

Under the TCJA, the favorable tax rates for long-term capital gains and qualified dividends were maintained, though the income thresholds for these rates were adjusted. In 2026, these rates themselves are not expected to change (0%, 15%, 20%), but the income thresholds at which they apply are tied to the ordinary income tax brackets. As ordinary income tax brackets revert to higher rates, the income thresholds for long-term capital gains and qualified dividends will also shift. This means that more investors could find themselves pushed into the higher 15% or 20% capital gains tax brackets, even if their total income hasn’t dramatically increased. Understanding these new thresholds will be crucial for tax-efficient portfolio management.

Net Investment Income Tax (NIIT)

The Net Investment Income Tax (NIIT) of 3.8% on certain investment income for high-income earners is a separate tax that was not directly altered by the TCJA and is not scheduled to sunset. This tax applies to the lesser of net investment income or the amount by which modified adjusted gross income (MAGI) exceeds certain thresholds ($200,000 for single filers, $250,000 for married filing jointly). While the NIIT itself isn’t changing, the interplay with potentially higher ordinary income tax rates and lower standard deductions means that more investors might find themselves subject to or more significantly impacted by the NIIT. Strategic tax planning will be essential to mitigate its effects.

Estate and Gift Tax Exemptions: Planning for Wealth Transfer

Wealthy investors and those engaged in estate planning face significant changes regarding estate and gift tax exemptions. The TCJA dramatically increased the estate and gift tax exemption amounts, offering unprecedented opportunities for tax-free wealth transfer. These generous exemptions are also set to revert.

Reversion of Estate and Gift Tax Exemption Amounts

In 2023, the federal estate and gift tax exemption is $12.92 million per individual, meaning a married couple can shield over $25 million from federal estate and gift taxes. In 2026, this exemption is projected to revert to approximately $5 million per individual (adjusted for inflation from its 2011 level). This drastic reduction will bring many more estates under the purview of federal estate tax, which carries a top rate of 40%. For investors with substantial assets, this change necessitates an urgent review of their estate plans. Strategies like making large gifts before 2026, establishing irrevocable trusts, or exploring other wealth transfer mechanisms should be considered to utilize the higher exemption while it’s still available.

Portability of Deceased Spousal Unused Exclusion (DSUE)

The concept of portability, which allows a surviving spouse to use any unused portion of a deceased spouse’s estate tax exemption, is a permanent feature of the tax code and is not set to expire. However, with the overall exemption amount reverting, the value of the DSUE will also decrease. This means that while portability remains, the amount that can be ported will be significantly less, further emphasizing the need for proactive estate planning in light of the reduced exemption.

Other Key Tax Considerations for Investors in 2026

Beyond the major shifts in individual income, capital gains, and estate taxes, several other areas will be affected by the 2026 US Tax Changes that investors need to monitor closely.

Qualified Business Income (QBI) Deduction (Section 199A)

The Section 199A deduction, also known as the Qualified Business Income (QBI) deduction, allows eligible self-employed individuals and owners of pass-through entities (S-corps, partnerships, LLCs) to deduct up to 20% of their qualified business income. This deduction was a significant benefit for many business owners and investors in pass-through entities. Crucially, the QBI deduction is also a temporary TCJA provision set to expire at the end of 2025. Its expiration in 2026 will mean a substantial increase in taxable income for many business owners, impacting their overall investment capacity and post-tax returns from their businesses. Investors with holdings in pass-through entities should model the impact of this deduction’s disappearance on their net income.

Alternative Minimum Tax (AMT)

The TCJA significantly curtailed the reach of the Alternative Minimum Tax (AMT) by increasing exemption amounts and phasing out thresholds. While the AMT itself is a permanent fixture, its applicability was greatly reduced for many taxpayers. As individual tax rates and deductions revert, the AMT might once again affect a broader range of high-income earners and investors. The AMT is a parallel tax system designed to ensure that wealthy individuals pay a minimum amount of tax, regardless of deductions and credits. Investors should be aware that certain tax-preferenced items, like incentive stock options (ISOs) or certain municipal bond interest, can trigger AMT liability.

Impact on Retirement Planning and Savings

While direct changes to 401(k) and IRA contribution limits are typically inflation-adjusted and not subject to the TCJA sunset, the overall tax environment influences retirement planning. Higher ordinary income tax rates in 2026 could make tax-deferred accounts (like traditional 401(k)s and IRAs) even more attractive, as contributions reduce current taxable income at potentially higher rates. Conversely, a potential future reduction in tax rates (if new legislation were passed) might favor Roth contributions. Investors should re-evaluate their retirement savings strategies in light of the changing tax brackets, considering the timing of contributions and withdrawals, and the balance between tax-deferred and tax-free growth accounts.

Strategic Planning for Investors: Actions to Take Now

Given the certainty of these upcoming 2026 US Tax Changes, proactive planning is not just advisable; it’s essential. Investors have a window of opportunity to optimize their financial strategies before the new rules take effect.

Review Your Investment Portfolio

Conduct a thorough review of your current investment portfolio. Identify assets that might be significantly impacted by changes in capital gains rates or the NIIT. Consider tax-loss harvesting strategies before the end of 2025 to offset gains. Rebalance your portfolio to align with your risk tolerance and new tax considerations. For instance, if you anticipate higher ordinary income tax rates, you might consider increasing your allocation to municipal bonds, which offer tax-exempt interest, especially for those in high-tax brackets.

Accelerate Income or Defer Deductions

With the expectation of higher ordinary income tax rates in 2026, consider strategies to accelerate income into 2024 or 2025 if you anticipate being in a lower tax bracket now. This could involve realizing capital gains, converting traditional IRAs to Roth IRAs, or taking distributions from deferred compensation plans. Conversely, deferring deductions into 2026, when they might be more valuable against higher tax rates, could also be a wise move. This strategy requires careful analysis of your individual tax situation.

Evaluate Your Estate Plan

For individuals with substantial wealth, the impending reduction in the estate and gift tax exemption is a critical concern. Now is the time to consult with an estate planning attorney to utilize the higher exemption amounts before they revert. This could involve making significant lifetime gifts, establishing irrevocable trusts, or exploring other sophisticated wealth transfer strategies. The goal is to transfer as much wealth as possible tax-free under the current, more generous rules.

Consult with Tax and Financial Professionals

The complexity of these 2026 US Tax Changes underscores the importance of professional guidance. A qualified tax advisor and financial planner can provide personalized advice based on your unique financial situation, investment goals, and risk tolerance. They can help you model the potential impact of these changes, identify opportunities for tax optimization, and develop a comprehensive strategy that aligns with your long-term objectives. Don’t rely solely on general advice; seek tailored expertise.

Stay Informed and Flexible

While the sunset provisions are currently set to revert, the legislative landscape is always subject to change. New tax legislation could be introduced that alters or extends some of the TCJA provisions, or introduces entirely new tax policies. Investors should remain vigilant, staying informed about political developments and potential legislative actions that could further impact the tax code. Building flexibility into your financial plan will allow you to adapt quickly to any new changes that may arise.

Potential New Legislation and Future Outlook

It’s important to acknowledge that the current projection of 2026 US Tax Changes assumes no new legislative action. However, the political environment is dynamic, and there’s always a possibility of new tax laws being enacted before or during 2026. Different political parties often have different philosophies regarding taxation, and the outcome of future elections could significantly influence the tax landscape.

Proposals for Tax Reform

Various proposals for tax reform have been put forward by policymakers. These could include:

- Further adjustments to capital gains taxes: Some proposals suggest taxing capital gains at ordinary income rates for high-income earners.

- Changes to the corporate tax rate: While the corporate tax rate was permanently reduced by the TCJA, future legislation could seek to increase it, which could indirectly affect equity valuations and investor returns.

- Modifications to deductions and credits: Specific deductions or credits could be introduced, expanded, or eliminated, impacting various investor groups.

- Wealth taxes: While highly debated, proposals for wealth taxes on ultra-high-net-worth individuals have been discussed, which could fundamentally alter estate and gift planning.

Investors should monitor these discussions closely, as any new legislation could create additional layers of complexity or new planning opportunities. Maintaining a diversified portfolio and a flexible financial plan will be key to adapting to unforeseen legislative shifts.

Conclusion: Proactive Planning is Your Best Strategy

The 2026 US Tax Changes represent a significant juncture for investors. With the scheduled expiration of key TCJA provisions, a return to higher individual income tax rates, reduced standard deductions, and substantially lower estate and gift tax exemptions is highly probable. These shifts will have a direct and measurable impact on investment income, wealth transfer strategies, and overall financial planning.

The time to act is now. By understanding these impending changes, reviewing your current financial situation, and engaging with knowledgeable tax and financial professionals, you can proactively adjust your strategies. This includes optimizing your investment portfolio, considering the timing of income realization and deduction deferral, and critically re-evaluating your estate plan to leverage current exemptions. Staying informed about potential new legislation will also be crucial for maintaining an agile and efficient financial strategy.

Ultimately, navigating the 2026 tax landscape successfully will require diligence, foresight, and expert guidance. By taking these steps, investors can not only mitigate potential negative impacts but also identify new opportunities to optimize returns and secure their financial future in the face of evolving tax laws. Don’t wait until 2026 to start planning; the decisions you make today will shape your financial well-being tomorrow.