Maximize Your 401(k) in 2026: A Comprehensive Guide to Employer Matching

Anúncios

Welcome to the ultimate guide for optimizing your 401(k) in 2026, with a special focus on maximizing employer matching contributions. In today’s dynamic financial landscape, understanding and leveraging every aspect of your retirement plan is more crucial than ever. For many, the 401(k) is the cornerstone of their retirement savings, and the employer match is essentially free money – a powerful boost to your future financial security that you absolutely shouldn’t leave on the table.

Anúncios

This comprehensive article will walk you through everything you need to know, from the fundamental mechanics of a 401(k) and its matching programs to advanced strategies for ensuring you capture every possible dollar your employer offers. We’ll delve into the nuances of vesting schedules, contribution limits, investment choices, and how to adapt your strategy to economic changes. By the end of this guide, you’ll be equipped with the knowledge and actionable steps to make 2026 your best year yet for retirement savings.

Understanding Your 401(k) and the Power of the Employer Match

Before we dive into optimization, let’s establish a solid understanding of what a 401(k) is and why the employer match is such a significant benefit. A 401(k) is an employer-sponsored retirement savings plan that allows employees to save and invest for retirement on a tax-deferred basis. This means your contributions and their earnings grow tax-free until you withdraw them in retirement, at which point they are taxed as ordinary income. Some plans also offer a Roth 401(k) option, where contributions are made after-tax, but qualified withdrawals in retirement are tax-free.

The true magic, however, often lies in the 401(k) employer match. This is a benefit where your employer contributes money to your 401(k) plan based on your own contributions. It’s an incentive to encourage employees to save for retirement and is a core component of many compensation packages. The most common matching formulas are:

Anúncios

- Dollar-for-dollar match up to a certain percentage: For example, an employer might match 100% of your contributions up to 3% of your salary. If you earn $60,000 and contribute 3% ($1,800), your employer will also contribute $1,800.

- Fifty cents on the dollar up to a certain percentage: An employer might match 50% of your contributions up to 6% of your salary. If you contribute 6% ($3,600), your employer will contribute 3% ($1,800).

- Graduated match: Some employers have more complex formulas, matching a higher percentage for the first few percentage points and then a lower percentage for subsequent contributions.

Why is this ‘free money’ so important? Because it represents an immediate, guaranteed return on your investment. If your employer matches 100% of your contribution up to 3%, that’s an instant 100% return on that portion of your savings, before any market gains. Over decades, these matching contributions, compounded with your own investments, can add hundreds of thousands of dollars to your retirement nest egg. Ignoring the employer match is akin to turning down a significant pay raise.

Step-by-Step Guide to Maximizing Your 401(k) Employer Match in 2026

Now that you understand the immense value, let’s outline the practical steps to ensure you’re getting every penny of your 401(k) employer match in 2026.

Step 1: Understand Your Plan’s Specifics

The first and most critical step is to fully comprehend the details of your company’s 401(k) plan. Don’t assume anything. Obtain and review your plan document, often available through your HR department or the plan administrator’s website. Key information to look for includes:

- Matching Formula: What percentage of your contribution does your employer match, and up to what percentage of your salary? Is it dollar-for-dollar, 50 cents on the dollar, or something else?

- Vesting Schedule: This is crucial. Vesting refers to the ownership of your employer’s contributions. Some plans have immediate vesting, meaning the money is yours right away. Others have a cliff vesting schedule (e.g., 100% vested after 3 years) or a graded vesting schedule (e.g., 20% vested each year for 5 years). If you leave your company before you are fully vested, you might forfeit some or all of the employer’s contributions. Understanding your vesting schedule helps you make informed decisions, especially if you’re considering a job change.

- Contribution Limits: The IRS sets annual contribution limits for 401(k)s. For 2026, these limits will likely be similar to or slightly higher than previous years. Ensure your contributions, including the employer match, do not exceed these limits. Always check the latest IRS guidelines.

- Eligibility Requirements: Do you need to be employed for a certain period before you can contribute or receive the employer match? Are there age requirements?

Step 2: Contribute At Least Enough to Get the Full Match

This is the golden rule of 401(k) saving. If your employer matches 100% of your contributions up to 5% of your salary, you should aim to contribute at least 5% of your salary. If you contribute less, you are literally leaving free money on the table. If your budget is tight, prioritize this contribution above almost all other savings goals, as the immediate return from the match is unparalleled.

Step 3: Maximize Your Contributions Beyond the Match (If Possible)

Once you’ve secured the full 401(k) employer match, the next step is to contribute as much as you can up to the IRS annual limit. The more you contribute, the more your money can grow tax-deferred (or tax-free with a Roth 401(k)). Consider increasing your contribution percentage whenever you get a raise or a bonus. Even a small increase, say 1% or 2% each year, can significantly impact your long-term savings due to the power of compounding.

Step 4: Understand and Optimize Your Vesting Schedule

As mentioned, vesting determines when your employer’s contributions truly become yours. If you have a graded vesting schedule, you might want to consider the implications if you plan to leave your job. For example, if you are 60% vested after three years and plan to leave at three and a half years, you might consider staying for the full four years to become 80% vested, especially if the forfeited amount is substantial. Always weigh the financial benefits against your career goals and personal circumstances.

Step 5: Review and Adjust Your Contributions Annually

Your financial situation, income, and even the IRS contribution limits can change year to year. Make it a habit to review your 401(k) contributions and overall financial plan at least once a year, ideally at the beginning of the year or during your company’s open enrollment period. This ensures you’re always contributing the optimal amount to capture the full match and stay on track for your retirement goals.

Beyond the Match: Advanced 401(k) Optimization Strategies for 2026

Securing the 401(k) employer match is foundational, but there are further strategies to supercharge your retirement savings.

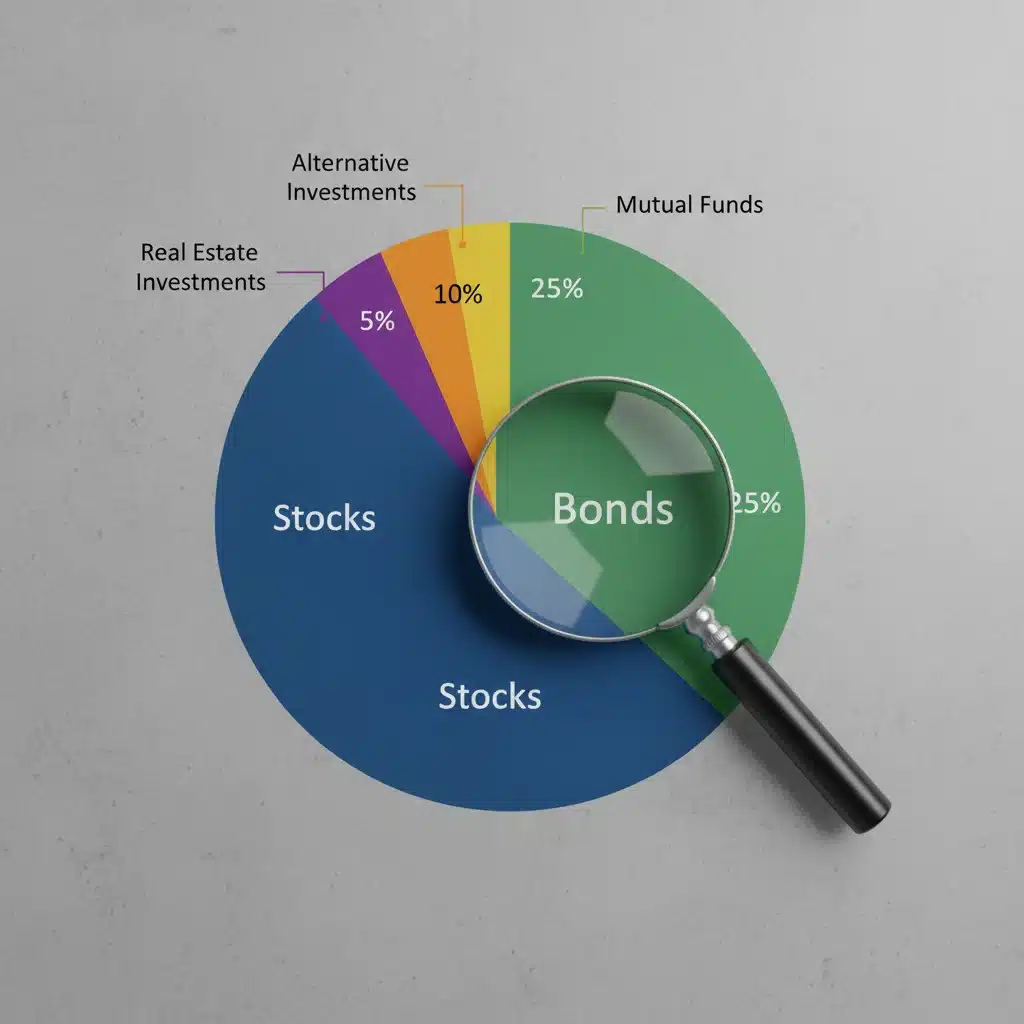

Strategy 1: Diversify Your Investments Within Your 401(k)

Your 401(k) plan typically offers a selection of investment options, such as target-date funds, index funds, mutual funds, and sometimes individual stocks or bonds. It’s crucial to diversify your investments across different asset classes to mitigate risk and optimize returns. A well-diversified portfolio balances risk and reward, ensuring that no single investment performs poorly enough to derail your overall retirement plan.

Consider your age, risk tolerance, and time horizon. Younger investors with a longer time horizon might opt for a more aggressive portfolio heavily weighted towards equities, which offer higher growth potential. As you approach retirement, you might gradually shift towards a more conservative allocation with a higher proportion of bonds and other less volatile assets to protect your accumulated wealth.

Strategy 2: Understand and Utilize Target-Date Funds

Many 401(k) plans offer target-date funds, which are designed to simplify investment decisions. These funds automatically adjust their asset allocation over time, becoming more conservative as you approach your target retirement date. For hands-off investors, target-date funds can be an excellent option, providing built-in diversification and rebalancing. However, always review the specific fund’s underlying holdings and expense ratios to ensure it aligns with your risk tolerance and financial goals.

Strategy 3: Consider a Roth 401(k) Option (If Available)

If your employer offers a Roth 401(k), it’s worth considering, especially if you expect to be in a higher tax bracket in retirement than you are now. Contributions to a Roth 401(k) are made with after-tax dollars, meaning your withdrawals in retirement are tax-free. This can be a significant advantage, particularly for younger individuals whose income is likely to grow over their careers. The employer match, however, will typically still be made to a pre-tax 401(k) account, even if you contribute to a Roth 401(k).

Strategy 4: Keep an Eye on Expense Ratios

Investment fees, particularly expense ratios of mutual funds and ETFs, can significantly eat into your returns over decades. Even a seemingly small difference in expense ratios (e.g., 0.5% vs. 1.5%) can translate into tens of thousands of dollars lost to fees over your lifetime. When selecting investment options within your 401(k), prioritize funds with lower expense ratios, especially for index funds and passively managed ETFs.

Strategy 5: Rebalance Your Portfolio Periodically

Over time, market fluctuations can cause your portfolio’s asset allocation to drift from your target. For instance, if stocks perform exceptionally well, they might come to represent a larger percentage of your portfolio than you initially intended. Rebalancing involves selling off some of your overperforming assets and buying more of your underperforming ones to restore your desired allocation. This helps maintain your risk profile and can even lead to buying low and selling high. Many experts recommend rebalancing annually or semi-annually.

Navigating Common 401(k) Challenges in 2026

Even with the best intentions, you might encounter challenges in maximizing your 401(k) employer match and overall savings. Here’s how to address some common hurdles:

Challenge 1: Limited Funds to Contribute

If you’re struggling to contribute enough to get the full employer match, it’s time for a budget overhaul. Look for areas where you can cut expenses, even temporarily. Consider a side hustle to generate extra income. Remember, the employer match is a guaranteed return, making it a top financial priority. Even if you can only contribute a small amount initially, aim to at least reach the match threshold.

Challenge 2: Confusing Investment Options

The array of investment choices in a 401(k) can be overwhelming. If you’re unsure, start with a target-date fund that aligns with your estimated retirement year. These funds offer a diversified, professionally managed approach. Alternatively, consider broad market index funds (e.g., S&P 500 index fund) for simplicity and low costs. Don’t let paralysis by analysis prevent you from investing.

Challenge 3: Job Changes and Rollovers

When you change jobs, you’ll have a few options for your old 401(k):

- Leave it with your old employer: This might be an option if you like the investment choices and fees, but it can make your financial planning more complex with multiple accounts.

- Roll it over into your new employer’s 401(k): This consolidates your accounts, simplifying management.

- Roll it over into an Individual Retirement Account (IRA): This often provides a wider range of investment options and potentially lower fees than an employer-sponsored plan.

- Cash it out: This is generally the worst option, as you’ll likely face income taxes and a 10% early withdrawal penalty if you’re under 59½ years old.

Always consult with a financial advisor before making a decision about an old 401(k) to ensure you choose the best path for your situation.

Challenge 4: Market Volatility and Emotional Investing

The stock market will have its ups and downs. It’s crucial to resist the urge to panic and make rash decisions during downturns. Time in the market, not timing the market, is key. Stick to your long-term investment strategy, continue to contribute consistently (especially when prices are lower), and remember that market corrections are a normal part of investing.

The Long-Term Impact of Maximizing Your 401(k) Employer Match

Let’s illustrate the profound impact of consistently maximizing your 401(k) employer match with a hypothetical example. Imagine a 25-year-old earning $60,000 annually, with an employer offering a 100% match on contributions up to 5% of their salary. They plan to retire at 65.

- Scenario A: No Employer Match (Contributing 0%) – This individual misses out entirely on the free money.

- Scenario B: Contributing to Get Full Match (Contributing 5%) – The individual contributes $3,000 annually (5% of $60,000), and the employer contributes an additional $3,000. Total annual contribution: $6,000.

Assuming a modest 7% average annual return, after 40 years:

- Scenario A: $0 (or only personal contributions if they contributed without the match).

- Scenario B: Approximately $1,197,000.

This simple example clearly shows that the employer match alone can be the difference between having almost nothing and becoming a millionaire by retirement. The power of compounding interest, amplified by those initial matching contributions, is truly remarkable.

Key Considerations for 2026 and Beyond

As we look to 2026, several factors might influence your 401(k) strategy:

- Inflation: Persistent inflation can erode the purchasing power of your savings. Ensure your investment strategy aims for returns that outpace inflation to maintain your future lifestyle.

- Interest Rate Environment: Higher interest rates can impact bond returns and potentially lead to shifts in equity valuations. Stay informed about economic trends and how they might affect your portfolio.

- Legislative Changes: Retirement plan rules can change. Stay updated on any potential legislative adjustments to contribution limits, catch-up contributions, or other 401(k) regulations that could impact your planning.

- Personal Financial Goals: Your life circumstances will evolve. Whether it’s buying a home, starting a family, or planning for a child’s education, ensure your 401(k) strategy remains aligned with your broader financial goals.

Conclusion: Make 2026 Your Best Retirement Savings Year

Maximizing your 401(k) employer match is not just a smart financial move; it’s a fundamental pillar of sound retirement planning. In 2026, commit to understanding your plan, contributing at least enough to capture every dollar of your employer’s match, and then pushing your contributions further if your budget allows. Diversify your investments, manage your fees, and stay disciplined through market fluctuations.

Your future self will thank you for the effort you put in today. By taking these proactive steps, you’re not just saving for retirement; you’re actively building a secure and prosperous future. Don’t let this invaluable benefit slip through your fingers. Take control of your 401(k) and unlock its full potential.