In the ever-evolving landscape of personal finance, staying ahead of tax law changes is not just about compliance; it’s about opportunity. As we look towards 2026, a new wave of tax credits and adjustments is on the horizon, presenting a significant chance for individuals and families to optimize their financial health. This comprehensive guide will delve into the intricacies of personal finance planning for 2026, focusing specifically on how leveraging these new 2026 Tax Credits can potentially save you up to $2,000 annually.

Understanding and strategically applying these tax credits can transform your financial outlook, allowing you to retain more of your hard-earned money. From clean energy incentives to family-focused deductions, the opportunities are diverse and impactful. Our goal is to equip you with the knowledge and actionable strategies needed to navigate the 2026 tax season with confidence and maximize your savings.

Anúncios

The financial world is dynamic, and tax codes are no exception. Each year brings new provisions, sunset clauses for older ones, and adjustments to existing regulations. For 2026, several key areas are expected to see significant changes, particularly concerning tax credits that aim to stimulate certain economic activities, support specific demographic groups, or encourage environmentally friendly practices. Proactive personal finance planning is crucial to capitalize on these shifts.

Ignoring these changes is akin to leaving money on the table. A well-informed approach to your finances, starting now, can ensure you are perfectly positioned to claim every eligible credit, thereby reducing your taxable income and boosting your refund or lowering your tax liability. Let’s embark on this journey to uncover the potential of 2026 Tax Credits and how they can be a cornerstone of your financial strategy.

Anúncios

The Shifting Landscape of 2026 Tax Credits: What to Expect

The year 2026 is poised to bring notable alterations to the tax code, influenced by legislative priorities, economic forecasts, and social objectives. While specific legislative details are still subject to change and finalization, we can anticipate certain themes and areas where new or expanded tax credits are likely to emerge or existing ones will be modified. These often revolve around national initiatives such as climate change, affordable healthcare, education, and support for families.

One of the most significant trends we’ve observed in recent years is the emphasis on green initiatives. Expect to see continued and potentially enhanced 2026 Tax Credits for energy-efficient home improvements, electric vehicle purchases, and renewable energy installations. These credits not only encourage sustainable living but also offer substantial financial incentives for taxpayers. For instance, upgrading your home insulation, installing solar panels, or purchasing an eligible EV could qualify you for thousands of dollars in credits, directly reducing your tax bill.

Another area of focus is often related to family and childcare. Policy discussions frequently include measures to ease the financial burden on working parents. While the expanded Child Tax Credit saw temporary enhancements in previous years, there’s always potential for new or modified credits aimed at childcare expenses, dependent care, or even specific educational investments. Keeping an eye on these developments will be vital for families planning their 2026 finances.

Healthcare costs remain a significant concern, and tax credits designed to offset these expenses or encourage health-related investments are also a possibility. This could include credits for health insurance premiums for certain income brackets, or even for specific medical expenses not covered by insurance. Staying informed about these potential credits can help you make more cost-effective decisions regarding your health and wellness.

Education is another perennial area for tax benefits. While existing credits like the American Opportunity Tax Credit and Lifetime Learning Credit are well-established, there might be new incentives or adjustments to these programs to make higher education more accessible or to support vocational training. For students and parents saving for college, understanding these nuances will be critical.

Beyond these broad categories, it’s also important to consider potential sunset provisions for existing credits. Some tax credits are designed with expiration dates, and knowing which ones might disappear or be reduced in 2026 is just as important as knowing which new ones will emerge. This foresight allows for strategic timing of major purchases or investments to maximize current benefits before they change.

To effectively leverage these potential 2026 Tax Credits, it’s not enough to simply react; proactive research and planning are paramount. Subscribing to tax news updates, consulting with financial advisors, and reviewing official IRS publications as they become available will be your best approach to staying informed and prepared. The financial landscape of 2026 offers both challenges and opportunities, and with the right strategy, you can turn potential complexities into significant savings.

Strategic Personal Finance Planning: Laying the Groundwork for 2026

Effective personal finance planning is a continuous process, but it becomes particularly critical when significant tax code changes are anticipated. For 2026, laying the groundwork now will ensure you are in the best possible position to capitalize on new tax credits. This involves a multi-faceted approach that includes budgeting, saving, investing, and regular financial reviews.

The first step in any robust financial plan is a clear understanding of your current financial situation. This means creating a detailed budget that tracks your income and expenses. Knowing where your money goes is fundamental to identifying areas where you can save more, which in turn can be directed towards investments or expenses that might qualify for 2026 Tax Credits. For example, if you plan to purchase an electric vehicle, understanding your current savings capacity helps you determine how much you can allocate towards a down payment or even the full purchase.

Saving intelligently is another cornerstone. Beyond an emergency fund, consider setting up dedicated savings accounts for specific goals that might intersect with future tax credits. For instance, if you anticipate significant home improvements that qualify for energy efficiency credits, starting a home improvement fund now can provide the necessary capital. Automating your savings ensures consistency and helps you build wealth without constant manual effort.

Investing wisely also plays a crucial role. Review your investment portfolio to ensure it aligns with your long-term financial goals and risk tolerance. Consider tax-advantaged accounts like 401(k)s, IRAs, and HSAs, which offer immediate tax deductions or tax-free growth, complementing any future tax credits. Diversification and regular rebalancing are key to a healthy investment strategy.

One of the most impactful aspects of proactive planning is anticipating major life events. Are you planning to buy a home, get married, have children, or go back to school before or during 2026? Each of these events can significantly impact your tax situation and eligibility for various credits. For example, the birth of a child could make you eligible for enhanced child tax credits, while a home purchase might open doors to mortgage interest deductions or first-time homebuyer credits if they are introduced or re-instated. Documenting these plans and discussing them with a financial advisor can help tailor your strategy.

Regular financial reviews are essential. At least once a year, preferably towards the end of the year, sit down and review your budget, savings, investments, and overall financial goals. This is also an opportune time to research upcoming tax law changes and adjust your strategy accordingly. For 2026, this means keeping a close watch on legislative updates throughout 2024 and 2025.

Finally, consider the power of professional guidance. A qualified financial advisor or tax professional can provide personalized advice, help you understand complex tax laws, and identify specific 2026 Tax Credits that apply to your unique situation. They can also assist with tax-loss harvesting, retirement planning, and estate planning, all of which contribute to a robust financial future. Don’t underestimate the value of expert insight in navigating the complexities of tax optimization.

Maximizing Your Savings: A Deep Dive into Key 2026 Tax Credits

To truly save up to $2,000 annually, it’s essential to understand the specific categories of 2026 Tax Credits that are likely to be available and how to qualify for them. While the precise details will emerge closer to 2026, we can anticipate several key areas based on current legislative trends and societal priorities. This section will explore these potential credit categories and provide actionable steps to prepare.

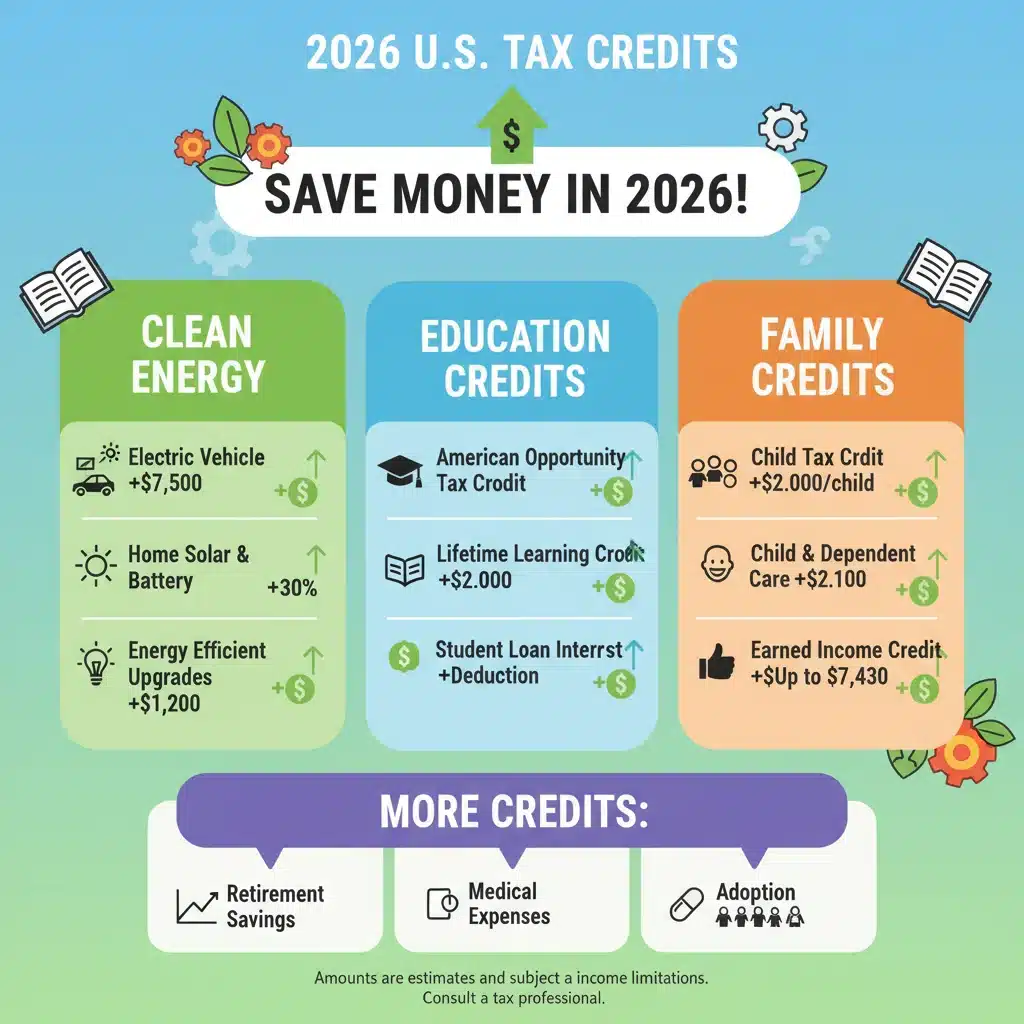

Clean Energy and Home Improvement Credits

The push for a greener economy is expected to continue impacting tax policy. 2026 Tax Credits for clean energy and home improvements are likely to remain a significant opportunity for savings. These credits often cover a percentage of the cost of eligible expenditures, such as:

- Solar Panels and Renewable Energy Systems: Installing solar, wind, or geothermal energy systems can often qualify for substantial credits. Keep detailed records of purchase and installation costs.

- Energy-Efficient Home Upgrades: This can include improvements like new energy-efficient windows, doors, insulation, or HVAC systems. These credits often have specific efficiency standards and caps on the amount you can claim. Research the efficiency ratings required for 2026.

- Electric Vehicle (EV) Credits: Federal and sometimes state-level credits for purchasing new or even used electric vehicles are a major incentive. These often depend on the vehicle’s manufacturing location, battery capacity, and the buyer’s income. If you’re considering an EV, start researching eligible models and income limitations now.

Actionable Step: If you’re planning any home renovations or a vehicle purchase, research the specific requirements for energy efficiency and eligibility well in advance. Keep all receipts, invoices, and manufacturer certifications. Consider getting energy audits to identify the most impactful upgrades.

Family and Dependent Care Credits

Support for families is a recurring theme in tax policy. While the specifics of the Child Tax Credit often fluctuate, expect continuing or new 2026 Tax Credits related to:

- Child Tax Credit (CTC): While the enhanced CTC from previous years has largely reverted, any new legislation could bring changes. Stay informed about income thresholds, child age requirements, and the maximum credit amount.

- Child and Dependent Care Credit: This credit helps offset the cost of care for children under 13 or dependents who cannot care for themselves. Keep meticulous records of childcare expenses, including the provider’s name, address, and Taxpayer Identification Number (TIN).

- Adoption Credit: This credit helps families with the costs associated with adopting a child. Document all qualified adoption expenses thoroughly.

Actionable Step: For families, maintaining detailed records of all childcare expenses, educational costs for dependents, and any adoption-related expenditures is crucial. Understand the income limits that may apply to these credits.

Education-Related Credits

Investing in education remains a priority, and 2026 Tax Credits for educational expenses will likely continue to play a significant role:

- American Opportunity Tax Credit (AOTC): For eligible students pursuing higher education, this credit can provide up to $2,500 per student for the first four years of post-secondary education. It requires enrollment at least half-time for at least one academic period.

- Lifetime Learning Credit (LLC): This credit offers up to $2,000 for courses taken towards a degree or to acquire job skills. It’s more flexible than the AOTC, applying to undergraduate, graduate, and professional degree courses.

- Student Loan Interest Deduction: While not a credit, this deduction can still significantly reduce your taxable income by allowing you to deduct interest paid on qualified student loans.

Actionable Step: Keep all education-related receipts, including tuition statements (Form 1098-T), book costs, and other required fees. Understand the income phase-outs for these credits, as they can limit eligibility.

Healthcare-Related Credits

While often less directly visible, credits related to healthcare can also offer savings:

- Premium Tax Credit (PTC): If you purchase health insurance through the Health Insurance Marketplace, you might be eligible for this credit, which helps lower your monthly premium costs. Eligibility is based on income and household size.

- Medical Expense Deduction: While not a credit, if your unreimbursed medical expenses exceed a certain percentage of your Adjusted Gross Income (AGI), you can deduct the amount over that threshold. This often applies to significant medical events.

Actionable Step: If you use the Health Insurance Marketplace, ensure your income information is up-to-date to receive the correct amount of advance premium tax credit. Track all medical expenses, especially if you anticipate high costs.

By proactively identifying which of these 2026 Tax Credits you might qualify for, and by meticulously documenting all relevant expenses and activities, you position yourself to maximize your annual savings. The potential to save up to $2,000, or even more, is a powerful incentive for diligent planning.

Navigating the Changes: Resources and Professional Guidance for 2026 Tax Credits

The complexity of tax codes means that staying informed and seeking expert advice are crucial, especially when anticipating changes like those expected for 2026 Tax Credits. Relying on accurate and up-to-date information is paramount to avoiding costly mistakes and ensuring you claim every credit you’re entitled to.

Official Resources

The most authoritative source for tax information is always the government itself. The Internal Revenue Service (IRS) website is an invaluable resource. As 2026 approaches, the IRS will release updated publications, forms, and guidance detailing new tax laws and credits. Regularly checking the IRS website for news releases, tax tips, and specific publications related to the upcoming tax year should be a standard part of your financial planning routine.

Beyond the IRS, state tax agencies also provide crucial information, as many states offer their own tax credits and deductions that can complement federal benefits. Your state’s department of revenue website will be the go-to place for state-specific tax law updates.

Legislative bodies, such as the U.S. Congress, also publish details of proposed and enacted tax legislation. Keeping an eye on financial news outlets that cover legislative developments can give you an early heads-up on potential changes, allowing you more time to adjust your financial strategy.

Leveraging Technology

Modern financial planning tools and tax software can significantly simplify the process of tracking expenses, organizing documents, and even identifying potential credits. Many budgeting apps allow you to categorize transactions, making it easier to pull reports for tax purposes. Tax preparation software, even for preliminary planning, can help you understand how different credits might impact your tax liability. While these tools are excellent aids, they are most effective when paired with a foundational understanding of tax principles.

The Role of Financial Professionals

For many, navigating the intricacies of tax law, especially with new 2026 Tax Credits on the horizon, can be overwhelming. This is where the expertise of financial professionals becomes indispensable.

- Certified Public Accountants (CPAs): CPAs are experts in tax law and can provide comprehensive tax planning and preparation services. They can help you understand how new credits apply to your specific situation, identify deductions you might overlook, and ensure compliance. Their advice can be particularly valuable for complex financial situations, small business owners, or those with significant investments.

- Enrolled Agents (EAs): EAs are tax specialists authorized by the U.S. Department of the Treasury to represent taxpayers before the IRS. They are highly knowledgeable about tax law and can offer excellent advice on tax planning and preparation.

- Financial Advisors: While not all financial advisors specialize in tax, many are well-versed in tax-efficient investing and overall financial planning. A good financial advisor can help integrate your tax strategy with your broader financial goals, ensuring that your investment decisions and major purchases align with potential tax benefits.

When choosing a professional, look for someone with experience in personal tax planning and who stays current with legislative changes. Don’t hesitate to ask about their qualifications, experience, and how they stay informed about new tax laws. A good professional relationship is built on trust and clear communication.

Proactive Documentation

Regardless of whether you use professional help, the responsibility of maintaining accurate records falls on you. Start now to organize your financial documents. Create a dedicated system for:

- Income statements (W-2s, 1099s)

- Investment statements

- Receipts for all potential credit-qualifying expenses (e.g., energy-efficient purchases, childcare, educational costs, medical bills)

- Loan interest statements (student loans, mortgages)

- Property tax statements

Digital copies are often easier to manage and store securely. Cloud storage, encrypted hard drives, or dedicated document management software can help keep your records organized and accessible. This meticulous record-keeping will not only simplify tax preparation but also provide solid evidence if your return is ever audited.

By actively utilizing official resources, leveraging technology, seeking professional guidance, and maintaining diligent records, you can confidently navigate the upcoming changes in 2026 Tax Credits. This proactive approach is not just about avoiding penalties; it’s about strategically positioning yourself to maximize your financial benefits and achieve your savings goals.

The Long-Term Impact of Leveraging 2026 Tax Credits on Your Financial Health

While the immediate goal of understanding and utilizing 2026 Tax Credits is to save money annually, the true power lies in their long-term impact on your overall financial health. Saving $2,000 a year, or even more, isn’t just a temporary boost; it’s an opportunity to build significant wealth over time through strategic reinvestment and debt reduction.

Accelerated Debt Reduction

One of the most impactful ways to use tax savings is to accelerate debt reduction. Whether it’s high-interest credit card debt, personal loans, or even your mortgage, channeling your tax savings into paying down principal can save you thousands in interest over the life of the loan. Imagine using that $2,000 annual saving to make extra mortgage payments; you could shave years off your loan term and free up significant cash flow in the future. This strategy not only reduces financial stress but also improves your credit score, opening doors to better financial opportunities.

Enhanced Savings and Investments

Alternatively, your tax savings can be a powerful engine for growing your wealth. Reinvesting that $2,000 into a diversified portfolio, a retirement account (like an IRA or 401(k)), or a college savings plan (like a 529 plan) can lead to substantial gains over time, thanks to the power of compound interest. For example, consistently investing an extra $2,000 annually over 20 years, assuming a modest 7% average annual return, could add over $80,000 to your nest egg. This illustrates how small, consistent savings, amplified by tax credits, can lead to significant financial independence.

Achieving Financial Goals Faster

Every dollar saved through 2026 Tax Credits brings you closer to your major financial goals. Whether it’s saving for a down payment on a house, funding a child’s education, starting a business, or planning for an early retirement, these savings provide the capital needed to turn aspirations into reality. By reducing your tax burden, you effectively increase your disposable income, which can then be strategically allocated to accelerate your progress towards these milestones.

Increased Financial Literacy and Confidence

The process of understanding and planning for 2026 Tax Credits also inherently increases your financial literacy. As you delve into tax laws, budgeting, and investment strategies, you gain a deeper understanding of how your money works and how to make it work harder for you. This enhanced knowledge translates into greater financial confidence, empowering you to make more informed decisions and take control of your financial future rather than feeling overwhelmed by it.

Building a Resilient Financial Future

Consistently leveraging tax credits and optimizing your finances builds a more resilient financial future. It creates a buffer against unexpected expenses, provides greater flexibility in career choices, and ultimately leads to a more secure retirement. By making smart tax decisions in 2026 and beyond, you are not just saving money for a single year; you are laying the foundation for lasting financial stability and prosperity for yourself and your family.

In conclusion, the 2026 Tax Credits offer more than just a temporary financial relief. They provide a strategic entry point for significant long-term financial growth. By embracing proactive planning, staying informed, and making judicious financial decisions, you can transform these annual savings into a powerful tool for achieving your most ambitious financial goals. Start planning today to unlock the full potential of these opportunities and secure a brighter financial tomorrow.